Rubrik.

A unique cybersecurity recovery company trading at a reasonable price-to-sales ratio

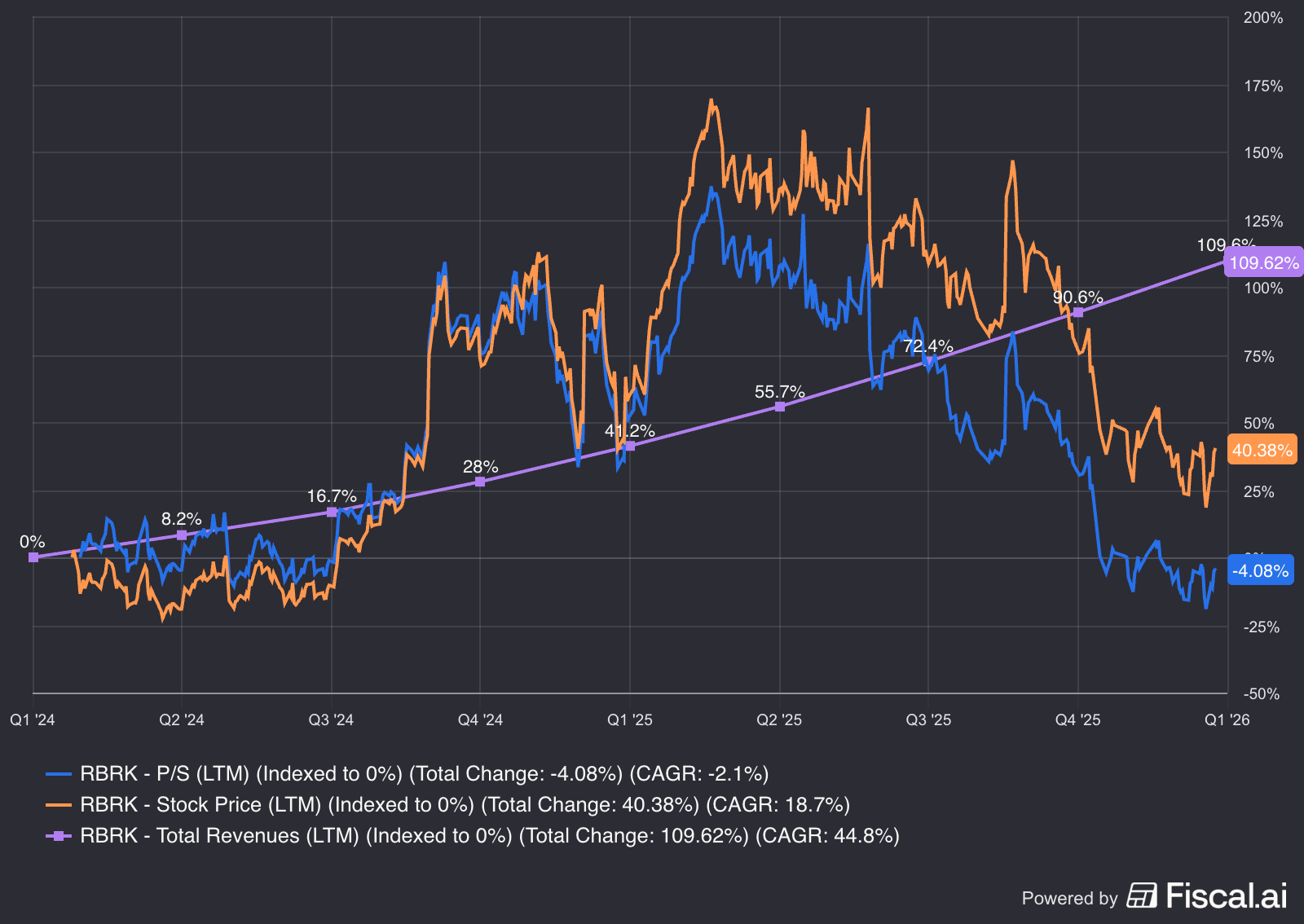

Rubrik ($RBRK) is currently trading at only 40% higher since its IPO day, despite more than doubling its revenue since. At today’s price, the stock trades at ~8-9x price-to-sales, a significant discount to cybersecurity peers that frequently command 15x or more.

The stock was trading at a 52-week low of ~$42-$43 just last week, which is admittedly a remarkable entry point at just ~6-7x P/S. It has rebounded since, partly lifted by ceasefire optimism from the US-Iran conflict.

Prior to that, the whole cybersecurity and SaaS sector has been undergoing a major selloff for more than several months, amplified by fears around AI disruption and most recently the Claude Mythos leak. The concern is that increasingly capable AI models could render traditional security vendors obsolete.

While Mythos claimed to have found significant vulnerabilities that humans overlooked, the sell off in cybersecurity names never made sense to me. Rubrik especially, has been actively using AI in its product.

The presence of AI for cyberattacks will also strengthen AI for cybersecurity.

Business Model

Rubrik sits at the intersection of data protection, cybersecurity, and enterprise software. Their flagship is the Rubrik Security Cloud, offered as a subscription-based platform spanning on-premises, cloud, and SaaS environments.

The company currently serves 6,100 customers including PepsiCo, The Home Depot, Allstate, GSK, and Carhartt.

Roughly one in three Fortune 500 companies rely on Rubrik to protect their data.

Assume Breach

Typical cybersecurity products are built around defence and prevention, keeping attackers out and shielding the system. Rubrik starts from a different assumption: breaches will happen.

The goal is to achieve Cyber Resilience: keeping data protected and operations running through an attack, and Cyber Recovery: restoring critical data and systems quickly.

No attackers will be able to hold your data or system hostage while demanding payment through cryptocurrency if your backups are untouchable and recovery takes hours instead of weeks.

Risks

Stock-Based Compensation

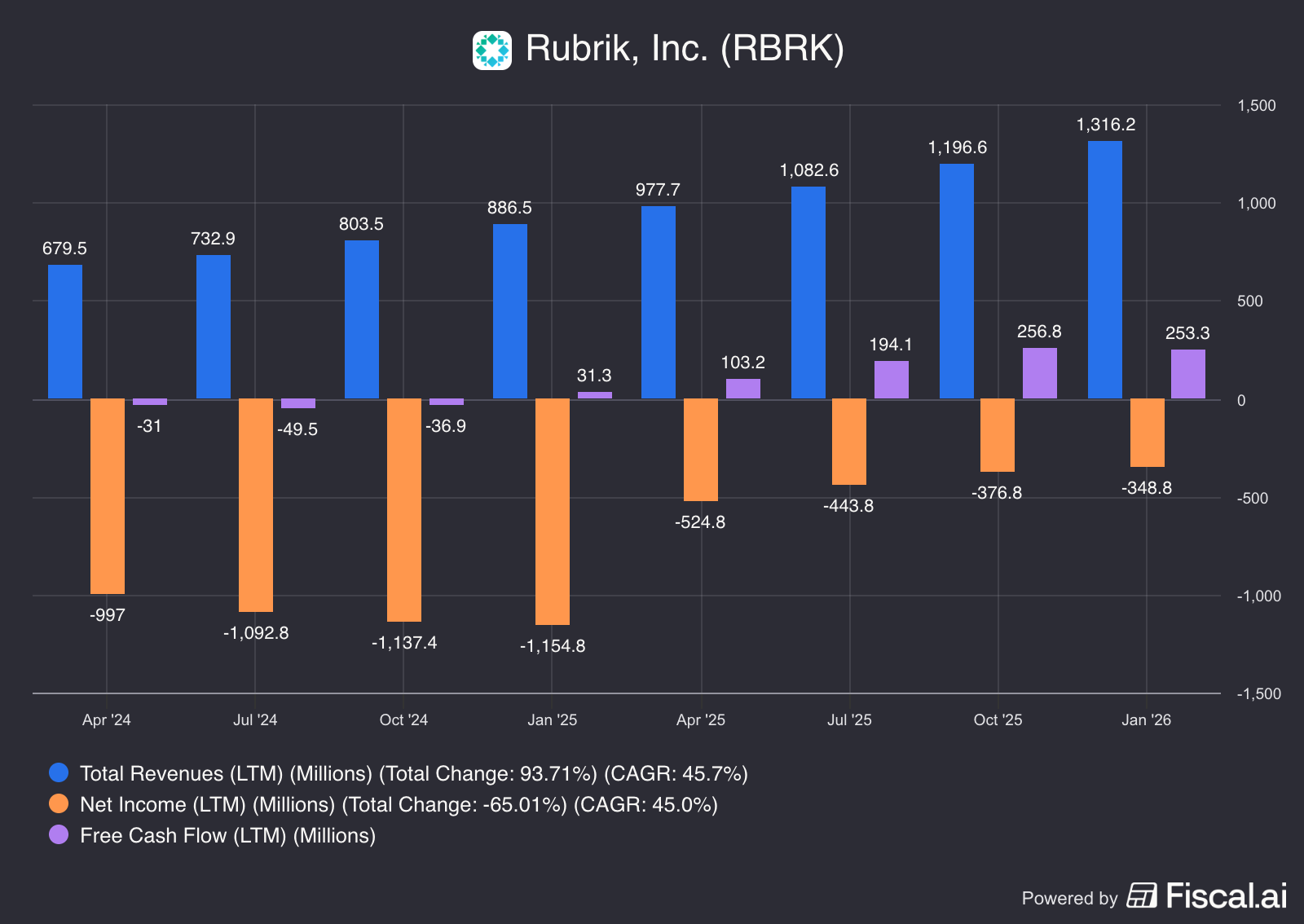

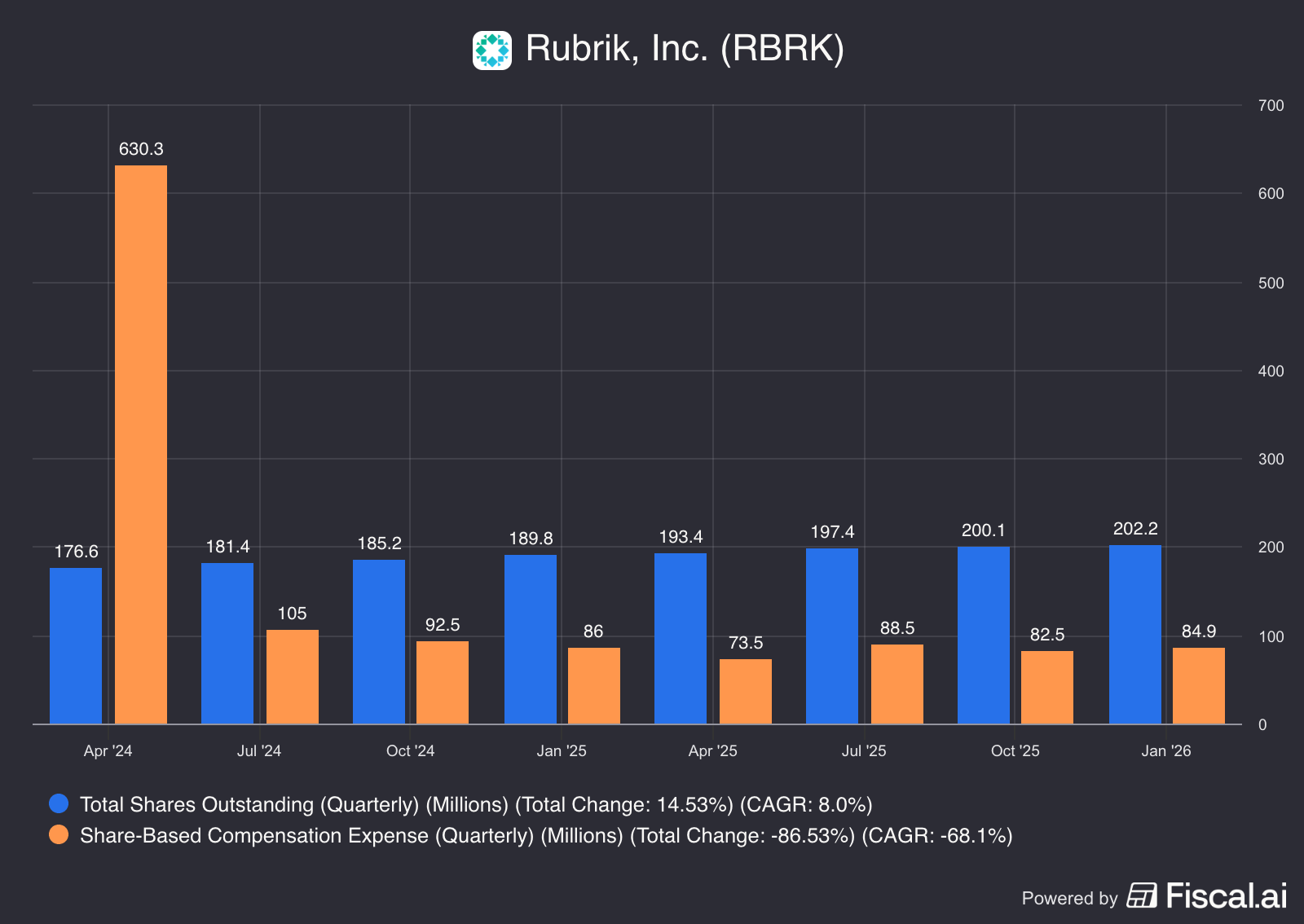

Rubrik recorded $329.4 million in SBC for the full fiscal year 2026, down significantly from $913.9 million in fiscal 2025. $329 million against roughly $1.3 billion in annual revenue means SBC is still running at around 25% of revenue.

That is meaningful dilution for shareholders, and the SBC is exactly why the company is still unprofitable on a GAAP basis.

Insider Selling

Over the past six months, insiders have traded RBRK 73 times, with 72 sales and just one purchase. The CFO alone sold 210,392 shares for roughly $11.5 million, while board member Ravi Mhatre sold 101,659 shares for approximately $8.3 million.

That is a lot of selling. The charitable read is that these are pre-scheduled 10b5-1 plans, standard practice for executives diversifying out of concentrated positions after an IPO lockup expires. The less charitable read is that the people who know the business best are not buying.

Final Thoughts

Rubrik occupies a part of the cybersecurity market that the big names do not primarily address. Detection and prevention are crowded: CrowdStrike, Palo Alto Networks, Cloudflare, and others compete aggressively for that layer. Recovery and resilience remain underserved. Commvault is the closest competitor, but growing at a fraction of Rubrik’s pace.

As enterprises scale their AI infrastructure and the threat surface widens, having an untouchable backup layer and a tested recovery plan is non-negotiable.

A third of Fortune 500 companies on your customer list is not something to take lightly. Enterprise procurement is slow, scrutinising, and unforgiving. That kind of penetration signals the product works, and that the solution is too important to ignore.

The heavy SBC is worth flagging, but also worth contextualising. Building a world-class engineering and security team means competing with the best companies in the world for talent. If that spend has bought Rubrik the people behind 34% ARR growth, 80%+ gross margins, and customers like GSK, PepsiCo, and The Home Depot, it is hard to argue it was unjustified. The trajectory is moving in the right direction.

The valuation assumes continued execution and declining SBC. But at 8-9x sales with this growth profile, in a category that gets more important every year, the risk-reward looks compelling.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice. Readers should conduct their own research before making any investment decisions.