Zscaler: Priced for Weakness

Leadership disruption created a valuation gap.

I have previously talked about Rubrik when it was trading at an attractive price-to-sales ratio. Now, another cybersecurity name has dropped into similar levels, at roughly 6 times revenue.

Zscaler is the leading zero trust security platform, protecting enterprise users and applications as they move to the cloud. The company serves over 9,400 customers across 185 countries, including approximately 40% of the Forbes Global 2000. Net Revenue Retention stood at 114% as of their last reported figure.

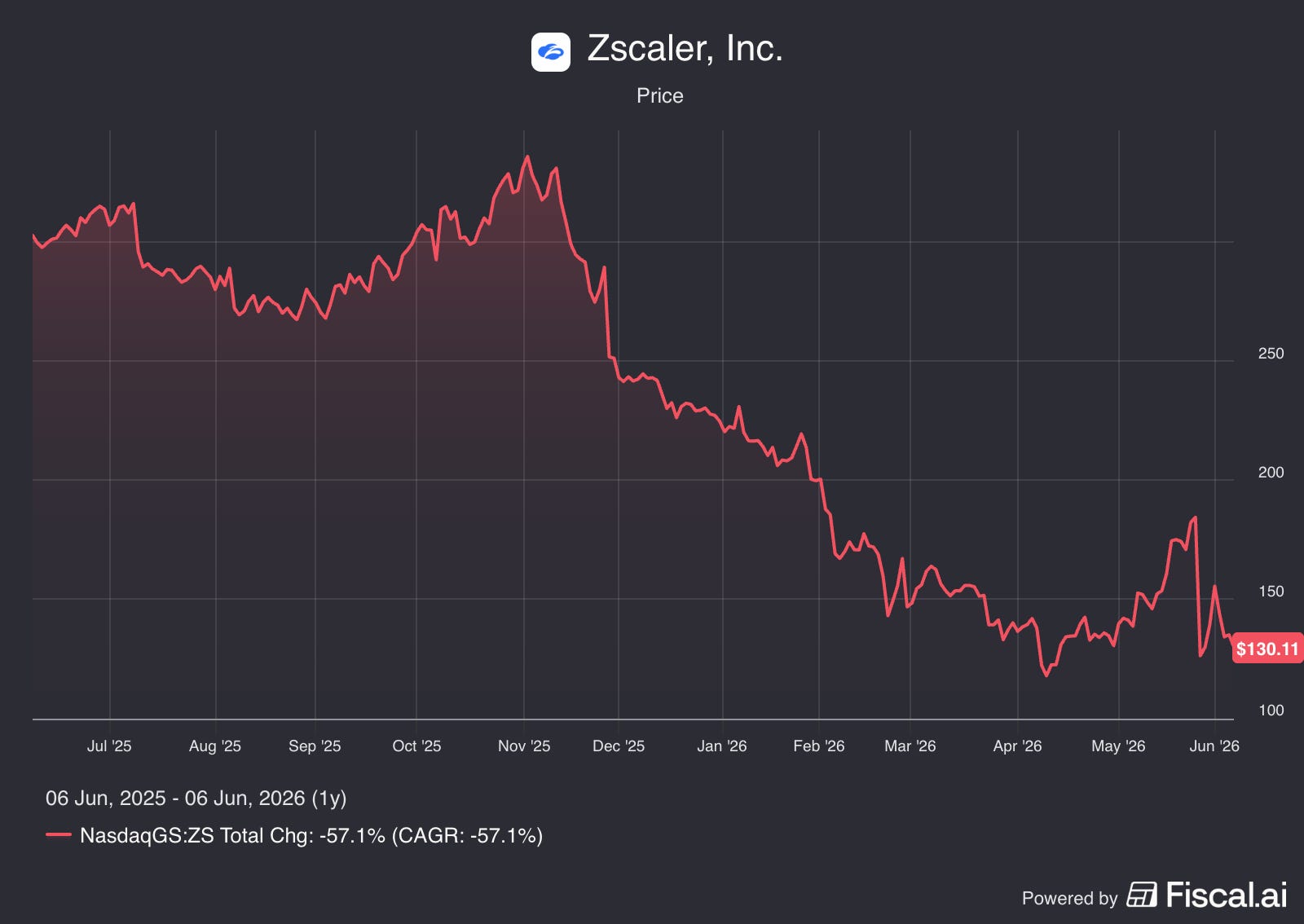

Zscaler shares dropped more than 50% in the past year since its peak of ~$336 a share.

The reasons can be summarised into two main points:

The Saaspocalypse was an industry-wide AI disruption, which annoyingly hit the cybersecurity sectors quite hard. If anything, AI should only strengthen the demand for cybersecurity services.

Then, in May, two unnamed sales leaders under the CRO left the company. Management took the prudent approach and guided for only 16%-17% growth for fiscal year 2027, below Wall Street expectations and a meaningful step down from FY 2026 ~24% growth.

Are sales leaders leaving such a big problem? Surely they can just replace the people and move on?

Enterprise software sales cycles are long, often 6–18 months. The relationships, pipeline knowledge, and deal momentum live with the salespeople. When two senior leaders walk out mid-cycle, disruption is guaranteed. Pipeline visibility, relationship with clients, everything needs to be re-accounted for and re-managed with new leaders and new people.

Valuation

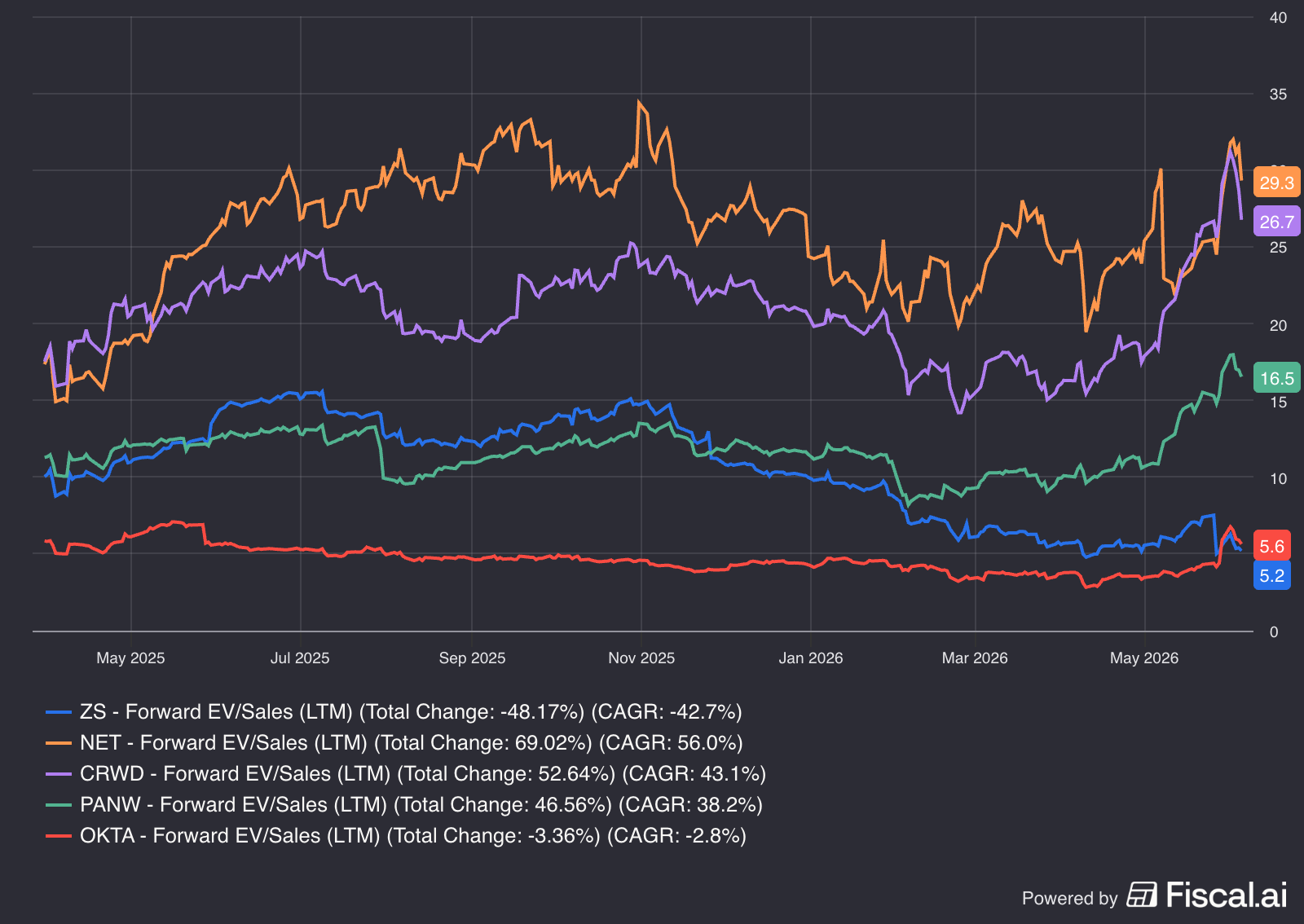

From a valuation standpoint, if we compare to peers:

Cloudflare (NET) is growing revenue at ~30–34%, and trades at ~29x forward EV/Sales

CrowdStrike (CRWD) is growing ARR at ~24–32%, and trades at ~26x EV/Sales

Palo Alto Networks (PANW) is growing revenue (organically) at ~14–15%, yet trades at ~16x forward EV/Sales

Okta (OKTA) is growing revenue at ~12%, and trades at ~5.6x forward EV/Sales

Zscaler (ZS) is guiding for 16%–17% growth, and trades at ~5.2x forward EV/Sales

The market is discounting Zscaler at 5.2x forward revenue, while Palo Alto Networks, growing at roughly the same rate, trades at 16x. PANW's stock even surged this year despite weaker underlying earnings.

Okta grew ~12% this year and guided for 9%-10% for FY 2027. This is slower than Zscaler's guided deceleration, and yet the two trades at a similar multiple.

If Okta deserves 5.6x forward EV/sales at sub-10% growth, why is Zscaler, guiding for 16–17%, priced similarly?

Final Thoughts

There is, of course, the risk that Zscaler management is hiding a much bigger problem in the leadership changes than what was implied in the earnings call. But the company fundamentals remain strong, and this is an attractive valuation for such a company.

If the sales organisation stabilises quicker than expected, it wouldn't be the first time a management team sandbagged guidance and beat it.

A prudent guidance can always be blown past.

And if the business performs in line with guidance, the downside at this multiple looks limited.

Disclaimer: I am not a financial advisor. This article is for informational and educational purposes only. It does not constitute financial advice. Readers should conduct their own research before making any investment decisions.